On chain settlement is frequently mentioned as a transformative concept, yet its meaning is often unclear to traditional financial institutions. The term can sound abstract or technical, leading to assumptions that it requires abandoning established systems. In practice, on chain settlement refers to how and where transactions are finalized, not to a wholesale replacement of financial infrastructure.

In 2026, traditional finance firms are approaching on chain settlement pragmatically. They are not adopting it for ideological reasons, but because it offers clearer settlement timing, improved transparency, and reduced operational friction. Understanding what on chain settlement actually does helps explain why institutions are experimenting with it in controlled and targeted ways.

On Chain Settlement Refers to Where Finality Occurs

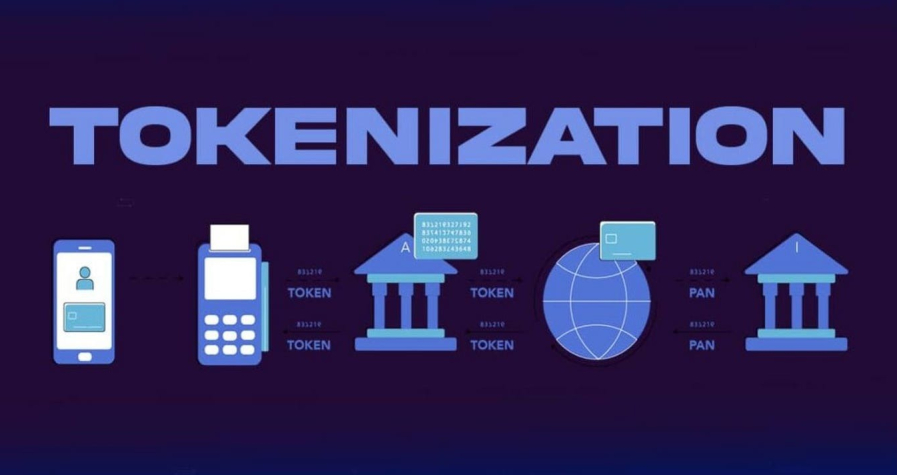

At its core, on chain settlement means that the final transfer of value and ownership is recorded and completed on a blockchain based ledger. Instead of relying on multiple internal databases and post trade reconciliation, settlement occurs on a shared system that all participants can observe.

For traditional finance, this does not mean removing legal agreements or custody structures. It means that the moment of settlement is synchronized and transparent. Once a transaction is confirmed on chain, ownership is updated and considered final within the defined framework.

This clarity around finality is one of the main reasons institutions are interested. Knowing exactly when settlement occurs reduces uncertainty and simplifies downstream processes.

How This Differs From Traditional Settlement Models

Traditional settlement models rely on sequential steps. Trades are executed, cleared, confirmed, and eventually settled, often across different systems and over multiple days. Each step introduces delay and counterparty exposure.

On chain settlement compresses these steps. Execution and settlement can occur closer together, sometimes within the same process. This reduces the time assets and funds remain in limbo.

For institutions, shorter settlement cycles lower counterparty risk and free up capital sooner. These benefits are operational rather than speculative, making them easier to justify internally.

Transparency and Shared Records Reduce Reconciliation

One of the hidden costs in traditional finance is reconciliation. Different parties maintain separate records that must be compared and corrected. Discrepancies require manual intervention and create operational risk.

On chain settlement provides a shared record. All authorized participants see the same transaction history and state changes. This reduces the need for repeated confirmation and reconciliation.

For finance teams, this transparency improves efficiency. Fewer breaks mean fewer exceptions to manage. Over time, this can significantly reduce operational overhead.

On Chain Does Not Mean Unregulated

A common misconception is that on chain settlement exists outside regulatory frameworks. In reality, institutions adopting on chain settlement do so within defined legal and compliance structures.

Permissions, access controls, and reporting requirements are built around the blockchain layer. On chain records can support audits and regulatory oversight rather than undermine them.

This alignment is critical. Institutions will not adopt settlement models that create legal ambiguity. On chain settlement is being designed to map to existing regulatory concepts such as ownership transfer and payment finality.

Integration With Existing Financial Systems

On chain settlement does not operate in isolation. Institutions integrate it with existing systems for custody, accounting, and risk management. The blockchain layer handles settlement, while other systems continue to perform their established roles.

This integration allows gradual adoption. Firms can apply on chain settlement to specific workflows without disrupting broader operations. Over time, successful use cases can be expanded.

The goal is not to replace everything at once, but to improve specific points of friction where traditional settlement is slow or complex.

Why Institutions Are Selective About Use Cases

Not every transaction benefits equally from on chain settlement. Institutions are selective, focusing on areas where timing and transparency matter most.

Use cases such as internal transfers, collateral movement, and cross border settlement are common starting points. These areas suffer from delays and fragmented processes that on chain settlement can improve.

This selectivity ensures that adoption is driven by measurable benefits rather than experimentation for its own sake.

Operational Risk Still Matters

While on chain settlement reduces some risks, it introduces others that institutions must manage. System reliability, governance, and access controls remain critical.

Institutions evaluate whether the settlement layer can operate consistently under stress. Downtime or unexpected behavior can disrupt operations just as much as delays in traditional systems.

As a result, on chain settlement is subject to rigorous testing and oversight. Reliability is a prerequisite for broader adoption.

Long Term Implications for Market Structure

As on chain settlement becomes more common, market structure evolves gradually. Settlement cycles shorten, transparency increases, and capital efficiency improves.

These changes do not create immediate disruption. Instead, they quietly reshape how markets function. Over time, this can influence liquidity, pricing, and participation.

For traditional finance, on chain settlement represents evolution rather than revolution. It modernizes processes without discarding foundational principles.

Conclusion

On chain settlement means that transaction finality occurs on a shared blockchain ledger, offering clearer timing, transparency, and efficiency. For traditional finance, it is not about replacing existing systems but about improving how settlement is executed. By integrating on chain settlement into specific workflows, institutions are modernizing infrastructure while maintaining regulatory and operational stability.