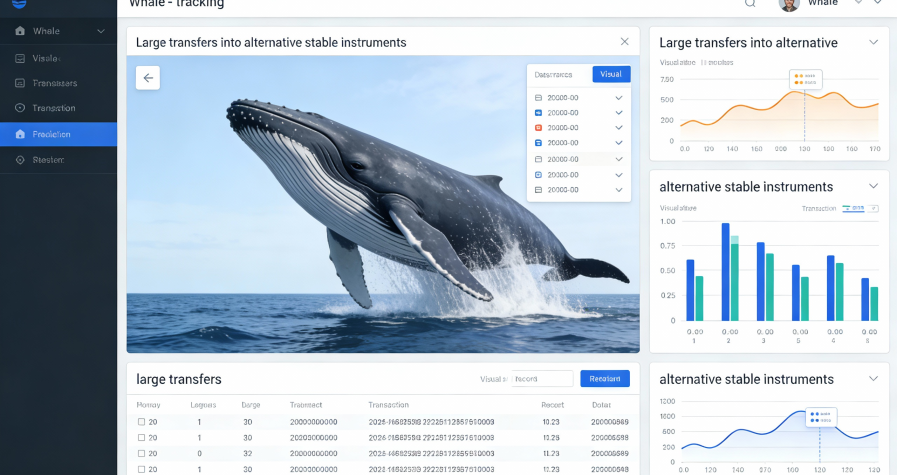

Stablecoins as Key Financial Tools

Issuers and payment firms are treating stablecoins less like a trading utility and more like programmable cash for settlement and treasury operations. Today, desks that once relied on bank cutoffs are routing dollars onchain to manage intraday liquidity, then reconciling positions back into fiat ledgers. The practical shift is about reducing failed payments and shortening cash conversion cycles, not chasing yield, and it is playing out across global finance in ways treasury teams can measure. Live monitoring of reserve movements and mint burn activity is also becoming standard in risk teams, especially when stress hits exchanges or OTC venues. Update notes from market makers now increasingly track stablecoin spreads alongside FX forwards, because both affect execution costs.

Integration into Global Finance

Enterprise adoption is being pulled forward by tokenization projects and cross-chain plumbing that makes stablecoins usable across venues. CoinDesk reported that Saudi Arabia is tokenizing parts of its economy, a framing that has pushed stablecoin settlement discussions into boardrooms that previously focused only on correspondent banking and reserve risk, as detailed in CoinDesk on Saudi tokenization and wealth protection. Today, compliance teams want clear line of sight on reserves, redemption windows, and sanctions screening before they approve any production flow. Live market chatter around Tether’s case, covered in Tether Faces Pressure to Unfreeze $344M in USDT, has also made treasury committees ask how freeze features and legal orders would work in their own payment stacks. Update cycles now include mapping counterparties and jurisdictions, not just blockchain uptime.

Impact on Traditional Banking Systems

Banks are being forced to compete on speed, transparency, and hours, because stablecoin rails do not close for weekends. Today, that pressure shows up in corporate treasury conversations about sweeping balances more frequently and holding smaller idle buffers. The operational angle is financial infrastructure, where reconciliation, fraud controls, and identity checks are being rebuilt for near-instant settlement, and bank product teams point to pilots like JPMorgan readies tokenized fund for stablecoin firms as evidence of institutional urgency. A useful comparison is how consumers expect immediate answers when searching walmart near me, which is the same expectation corporate clients now bring to payments status. Live bank pilots are increasingly judged by user experience and exception handling, and the Update cadence is measured in hours, not quarters.

Challenges and Regulatory Considerations

Regulators are focused on whether stablecoins should be treated like deposits, money market instruments, or a new category of payment token, because each choice changes capital, disclosure, and consumer protection. CoinDesk noted that a U.S. crypto market structure bill cleared a key hurdle, a reminder that legal definitions can shift quickly and affect listing, custody, and settlement workflows, as described in CoinDesk on the market structure bill movement. For global finance, the hardest problem is consistent supervision across borders when tokens circulate instantly and redemptions concentrate at a few gateways. Today, risk officers also track financial market infrastructure dependencies, such as stablecoin issuers relying on a narrow set of banks and custodians. Live enforcement actions and court orders create operational uncertainty, so Update procedures increasingly include playbooks for freezes, attestations, and rapid disclosures.

Future Outlook for Stablecoins in Finance

The next phase is likely to be defined by interoperability and clearer governance rather than by new token launches. Today, stablecoins that win enterprise flows will look boring: predictable redemption, robust compliance tooling, and integration into back-office systems that already handle cash, FX, and collateral. Invoices, payroll, trade finance, and merchant acquiring are increasingly in scope, and in global finance the key test is whether stablecoin settlement can be embedded into these flows without creating new points of failure. Live adoption will also depend on how quickly audit standards mature for reserves and how payment providers price instant finality versus chargeback-like protections. Update roadmaps from major venues now emphasize wallet risk controls, transaction screening, and standardized message formats, because those details determine whether stablecoins become routine plumbing or remain a specialist tool.